Many of the regulations introduced by the European Commission to help achieve its goal are laudable. The EU Taxonomy, for example, which aims to redirect capital towards economic activities classified as environmentally sustainable. The Sustainable Finance Disclosure Regulation (SFDR) should also aid asset owners' decision making by promoting transparency and standardisation, while also preventing greenwashing and making investors more accountable.

However, creating a single rulebook for a fast evolving and widely diversified sector like real estate is challenging and requires a more nuanced approach.

A particularly controversial piece of the new regulation is its more favourable treatment of new 'green' builds over decarbonising existing 'brown' buildings. The taxonomy currently lists energy renovations as a 'transitional activity' meaning they are not classified as wholly sustainable and therefore cannot be included in Article 9 funds i.e. those with environmental and / or social objectives. Instead, asset owners focused on Article 9 will only be able to invest in new builds, where significant embedded CO² emissions involved in construction are ignored.

This flawed logic is symptomatic of the regulation's inability to be used in a dynamic way. Sustainable investment commitments as defined under the SFDR – and the EU's action plan more broadly – only provide an ESG snapshot that promotes investment in a narrow set of activities considered sustainable today and hampers the wider adoption of others that could accelerate the transition to a more sustainable tomorrow.

Unintended consequences

For real estate investors it creates reputational risks as they are forced to make a decision on what are considered to be sustainable investments and perform the relevant – but subjective – checks. Another downside is the increased reporting burden and associated costs which can disproportionately impact smaller investors who are often the most active in engaging with real estate companies to help drive positive change.

The static nature of SFDR is also ill-suited to a sector reliant on patient capital. Its snapshot approach is problematic for long-term investors as sustainability improvements over time can have a hugely positive financial impact and often form a key part of our investment thesis.

More serious is the risk of unintended consequences for the allocation of capital by encouraging the demolition and rebuilding of real estate assets over the development of existing ones. According to the International Energy Agency (IEA), for the sector to decarbonise in line with 1.5°C of global warming, 50% of all current buildings need to be net zero by 2040, increasing to 85% by 2050. Starving these structures of the financing they require to achieve this is potentially harmful for the green transition.

Finally, asset owners may simply decide that real estate as an asset class is too complicated and avoid allocating altogether, as has been evidenced by the significant outflow from Article 9 strategies.

For the financial industry to play its part, it is vital that regulations bring investors on board rather than scaring them away. Similarly perplexing is that despite the explosion of green ratings for real estate – around 600 different systems at the last count – there is no regulatory or ESG data solution that assesses physical adaptation to increasing climate risks.

Huge investment opportunities

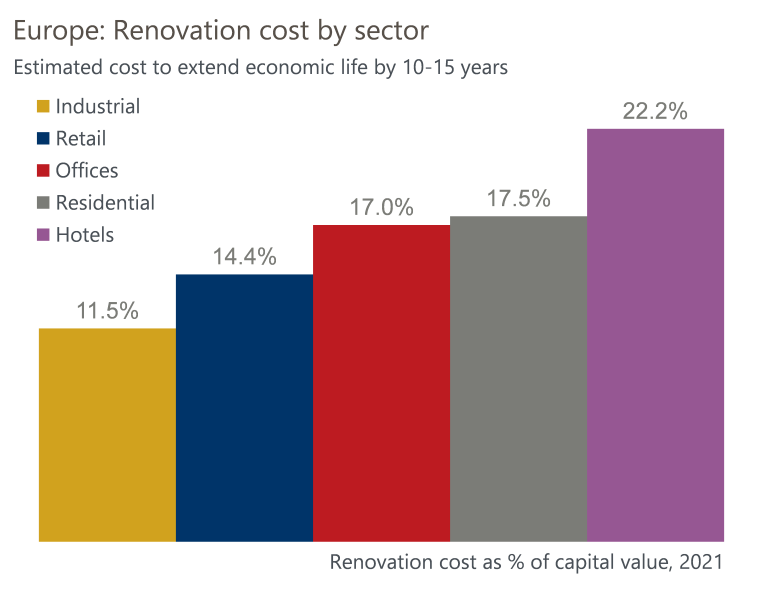

The renovations required to decarbonise our existing buildings will increase costs across most European real estate markets. A report by Oxford Economics estimated that renovating a property to extend its economic life by only 10-15 years could cost up to 30% of its capital value [1]. This has significant implications for investors, particularly in sub-sectors like hotels where buildings are often older, in prime locations and with high levels of energy intensity. Conversely, portfolios tilted towards industrial and retail assets will incur relatively smaller costs.

On a country level, investors in the UK – where minimum EPC standards are set to rise from 2027 – are expected to bear the highest renovation costs due to labour market inflation whereas Nordic countries will require the smallest investment given their lower obsolescence risk and capex ratios.

The increase in regulatory scrutiny means that these pressures will only increase and it is important that investors understand these factors. It supports a bottom-up approach to portfolio construction, built on detailed company understanding of the sustainability risks they face. It also creates huge investment opportunities, for example in solution companies enabling the transition.

In conclusion, sustainability has been one of our long-term portfolio themes. The real estate sector has many favourable ESG characteristics, including strong environmental management systems, innovation and a clear social contribution. The investment thesis is also simple – more sustainable properties will benefit from higher occupancy rates and the rent that tenants are willing to pay. This applies to both the construction of new assets and developing existing ones.

Real estate punches well above its financial weight in terms of CO² emissions and so has an important role to play in driving positive environmental change, both by reducing its own carbon footprint and setting an example for other sectors. The current regulatory categorisations, however, risk undermining these efforts by diverting much-needed capital away from transitional strategies. A more tailored approach is needed if the EU is to achieve its important decarbonisation targets that we all hope to see met.

***

Sources

[1] Oxford Economics, The renovation race to net-zero, April 2022

This is a marketing communication, and this document is intended for institutional investors. Alternative investment funds are only eligible for professional investors. Except otherwise stated, the source of all information is Storebrand Asset Management AS as at April 14 2023. Statements reflect the portfolio managers’ viewpoint at a given time, and this viewpoint may be changed without notice. Historical returns are no guarantee for future returns. Future returns will depend, inter alia, on market developments, the fund manager’s skills, the fund’s risk profile and subscription and management fees. The return may become negative as a result of negative price developments. Future fund performance is subject to taxation which depends on the personal situation of each investor, and which may change in the future. Storebrand Asset Management AS is a management company authorised by the Norwegian supervisory authority, Finanstilsynet, for the management of UCITS under the Norwegian Act on Securities Funds. Storebrand Asset Management AS is part of the Storebrand Group. No offer to purchase shares can be made or accepted prior to receipt by the offeree of the fund's prospectus and KIID and the completion of all appropriate documentation. For all fund documentation including the KIID, the Prospectus, the Annual Report and Half Year Report, unit holder information and the prices of the units, please refer to https://www.storebrand.com/sam/international/asset-management/. No offer to purchase shares can be made or accepted in countries where a fund is not authorized for marketing. Investors’ rights to complain and certain information on redress mechanisms are made available to investors pursuant to our complaints handling policy and procedure. The summary of investor rights in English is available here: https://www.storebrand.com/sam/international/asset-management/. Storebrand Asset Management AS may terminate arrangements for marketing under the Cross-border Distribution Directive denotification process.